The Smart Guide to Choosing Between Employer Health Insurance and Private PPO Plans

Before You Automatically Say “Yes” to Your Employer Plan…

If you’re like most people, you probably assume your employer health insurance is your best—or only—option.

But here’s the truth:

That’s not always the case.

If you’re relatively healthy, you may be overpaying for coverage that doesn’t actually fit your lifestyle… while missing out on options that could offer:

Lower monthly premiums

More flexibility

Nationwide access to doctors

This guide will help you understand when it actually makes sense to consider a private underwritten PPO plan—and when it doesn’t.

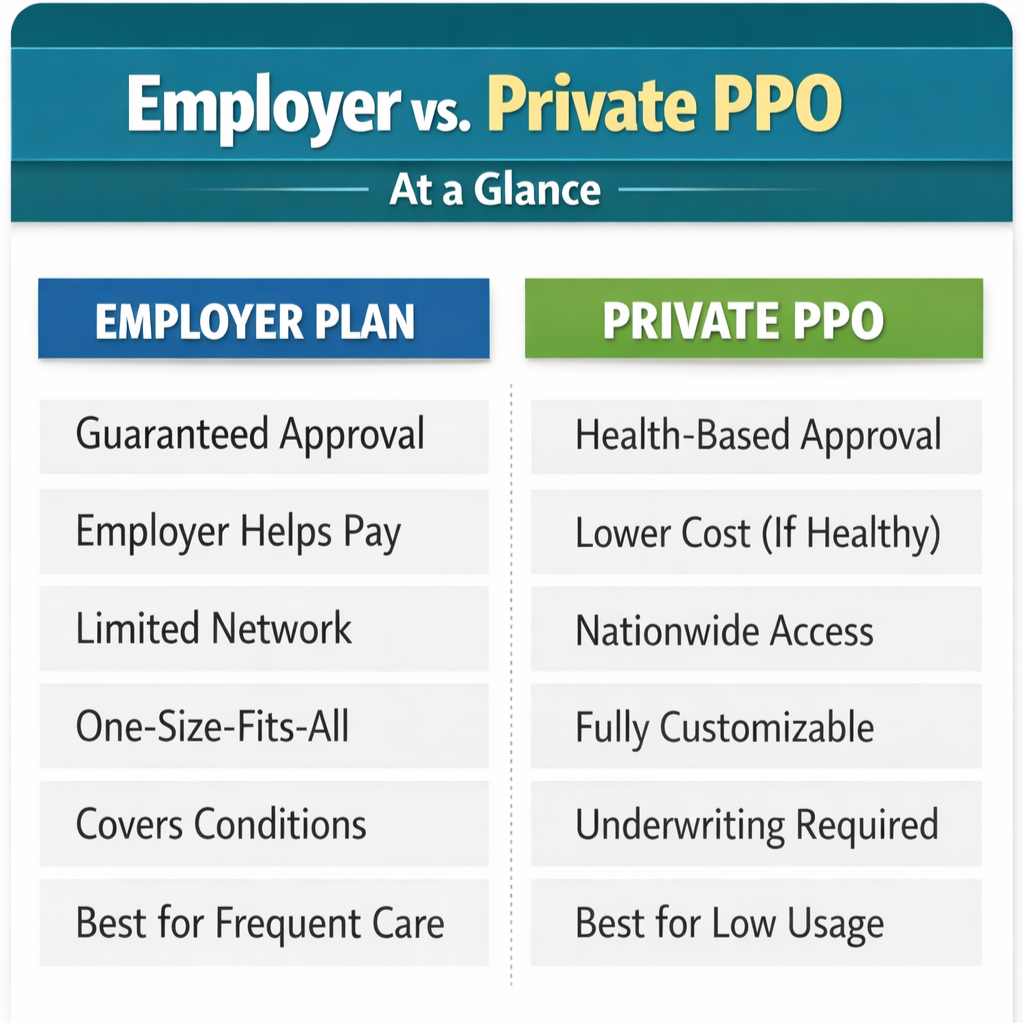

First—What’s the Difference?

Employer Health Insurance

No health questions (guaranteed approval)

Employer may cover part of the cost

Often limited networks (HMO or regional plans)

One-size-fits-all coverage

Private Underwritten PPO Plans

Requires approval based on health

Typically designed for healthy individuals

Offers nationwide PPO access

Fully customizable to your needs

When a Private PPO Plan Might Be the Better Fit

✅ 1. You’re Healthy and Don’t Use Insurance Often

If you:

Rarely go to the doctor

Don’t have chronic conditions

Aren’t on expensive medications

You could be paying for more coverage than you actually use.

Private PPO plans often reward good health with lower monthly costs.

✅ 2. Your Employer Plan Feels Expensive (Especially for Family)

This is one of the biggest reasons people explore alternatives.

Employers often:

Help pay for your premium

But pass most of the cost to your spouse and kids

That’s where costs can skyrocket.

In many cases, families can find better pricing and flexibility outside the employer plan.

✅ 3. You Need Nationwide Coverage

If your lifestyle includes:

Traveling for work

Living in multiple states

Wanting freedom to choose doctors

Employer plans can feel restrictive.

Private PPO plans typically allow you to:

See providers across the country

Skip referrals to specialists

Keep consistent coverage wherever you go

✅ 4. You’re Self-Employed or 1099

If you don’t have access to an employer plan, you’ve likely seen marketplace options that are:

Expensive

Limited in network access

Not very flexible

If you’re healthy, a private PPO plan may offer:

Better pricing

Stronger networks

More control over your coverage

✅ 5. You Want Control Over Your Plan

Employer plans are designed for groups—not individuals.

With a private plan, you can:

Choose your deductible

Adjust your coverage

Build a plan that actually fits your life

When You Should Stay With Your Employer Plan

Let’s be clear—private PPO plans are not for everyone.

Here’s when sticking with your employer plan is usually the smarter move:

🚫 You Have Pre-Existing Conditions

Private plans require medical approval.

Employer plans:

Accept everyone

Cover pre-existing conditions

🚫 Your Employer Pays Most of the Premium

If your employer heavily subsidizes your plan, it can be hard to beat financially.

🚫 You Need Frequent or Ongoing Care

If you:

See doctors regularly

Need ongoing treatments

Rely on expensive prescriptions

A traditional plan may offer more predictable coverage.

The Simple Decision Framework

Use this as a quick gut-check:

👉 Consider a Private PPO if:

You’re healthy

You want lower monthly costs

You value flexibility and nationwide access

👉 Stick With Employer Coverage if:

You have ongoing health conditions

Your employer covers a large portion of your premium

You need consistent, frequent care

The Biggest Mistake People Make

Most people don’t compare.

They assume:

“My employer plan must be the best option.”

But without looking at alternatives, you may be:

Overpaying.

Over-insured in areas you DON’T use.

Underutilizing better options available to you.

Want to Know What Actually Makes Sense for You?

The right plan depends on:

Your health.

Your budget.

Your lifestyle.

Your risk tolerance.

A quick comparison can help you see your options clearly—without the confusion.

👉 Next Step

If you’re curious whether a private PPO plan could be a better fit, the best next step is a simple, no-pressure review.

You’ll walk away knowing:

What you currently have

What else is available

What actually makes the most sense for your situation

Because the right health insurance plan shouldn’t just be what’s offered…

it should be what fits your life.