Don’t Qualify for ACA Subsidy? Consider Private Health Insurance Plans

Not everyone qualifies for Marketplace subsidies—and that doesn’t mean you’re out of options. Many individuals and families earn “too much” to receive financial assistance through the ACA Marketplace, yet still face frustratingly high monthly premiums.

The good news? Private health insurance plans can be a strong alternative when subsidies aren’t available—especially for healthy individuals, self-employed professionals, and families looking for more affordable coverage.

Why Some People Don’t Qualify for Marketplace Subsidies (Premium Tax Credits)

ACA Marketplace subsidies are income-based and designed to help lower- and middle-income households afford coverage. You may not qualify if:

Your income exceeds the subsidy threshold (above 400% FPL /Federal Poverty Level)

You’re self-employed with fluctuating income

Your employer offers comprehensive, "affordable" coverage – which means that it pays for 60% of a standard population's average healthcare costs

You earn less than 100% of the federal poverty level (FPL).

Your tax filing status disqualifies assistance.

You're not legally present in the U.S., or you're incarcerated

If you are in the coverage gap population: uninsured adults with incomes above the state's current Medicaid eligibility level but below the poverty level who fall into a "coverage gap" of earning too much to qualify for Medicaid but not enough to qualify for tax credits.

Citizenship status: Undocumented immigrants are barred from purchasing coverage through the Marketplace even without financial assistance.

When subsidies aren’t available, Marketplace plans can become expensive—often combining high premiums with high deductibles, making coverage feel unaffordable for those who rarely use medical services. (I hear this all the time).

What Are Private Health Insurance Plans?

Private health insurance plans are non-Marketplace plans offered through insurance carriers using medical underwriting. Unlike ACA plans, these policies are not income-based and do not rely on subsidies to remain affordable.

Instead, eligibility and pricing are based on factors such as age, overall health, and coverage needs. These plans are often ideal for individuals who are in good health and want more control over their monthly costs and plan design.

Benefits of Private Health Insurance

For those who qualify, private health insurance can offer several key advantages:

Lower Monthly Premiums

Private plans often cost significantly less per month than unsubsidized Marketplace plans, especially for healthy individuals.

Flexible Coverage Options

Many private plans allow you to customize coverage—so you’re not paying for benefits you may never use.

Short-Term and Long-Term Solutions

Depending on the plan, coverage can range from temporary protection to longer-term options with renewability features.

Access to Broad or Nationwide Networks

Some private plans include PPO or nationwide provider networks, making them a good fit for travelers, remote workers, or those who want more provider flexibility.

Who Is a Good Candidate for Private Health Insurance?

Private health insurance may be a great fit if you:

Are generally healthy

Don’t qualify for Marketplace subsidies

Are self-employed or a 1099 contractor (tax write-off ..yes, please)

Want lower premiums and predictable costs

Missed Open Enrollment and don’t qualify for a Special Enrollment Period.

Wants first dollar benefits, meaning the plan will start covering a percentage% before meeting a deductible.

It’s important to note that most private plans require medical underwriting, meaning approval is based on health history.

Managing High Deductibles Strategically

Some private plans include higher deductibles—but this doesn’t have to be a drawback when planned correctly.

Many individuals pair private health insurance with supplemental coverage designed to help offset out-of-pocket costs related to:

Hospitalizations

Emergency room visits

Unexpected illnesses or accidents

This layered approach can provide strong catastrophic protection while keeping monthly costs lower than traditional unsubsidized ACA plans.

Dental and Vision Coverage Options

Unlike many Marketplace plans, private insurance options may offer:

Stand-alone dental plans

Vision coverage

Bundled benefit packages

This allows you to customize coverage based on your needs—without paying for benefits you don’t use.

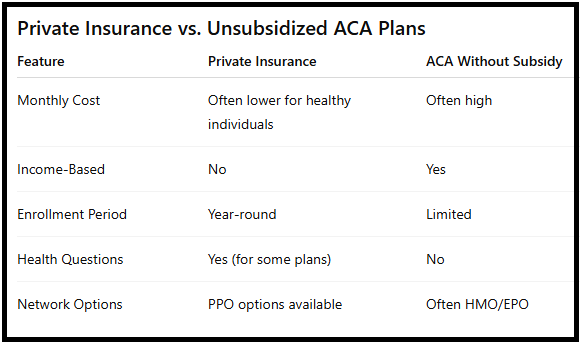

Private Insurance vs. Unsubsidized Marketplace Plans

Private Insurance vs. ACA without subsidy differences.

Choosing the Right Plan Matters

Private health insurance is not one-size-fits-all. Choosing the wrong plan—or going without professional guidance—can lead to coverage gaps or unexpected expenses.

Working with a licensed health insurance professional helps ensure that:

You understand what’s covered (and what’s not)

You’re matched with plans you actually qualify for

Your coverage aligns with your health needs and budget

Final Thoughts

If you don’t qualify for Marketplace subsidies, you still have options. Private health insurance plans can provide affordable, flexible coverage—especially when paired with supplemental protection to manage out-of-pocket costs.

The key is understanding your choices and selecting a plan that truly fits your situation.

If you’re unsure where to start, personalized guidance can make all the difference.

References

https://www.healthinsurance.org

https://www.irs.gov/affordable-care-act/

https://www.kff.org/affordable-care-act/